I thought we had it all figured out. My dad worked 43 years at the same job. He saved his money. He owned a home. He had a will.

But when he got sick with cancer, I did what most daughters would. I got help. I followed the advice I was given, and focused on caring for him. I was told the house wouldn't be at risk and everything would be fine…

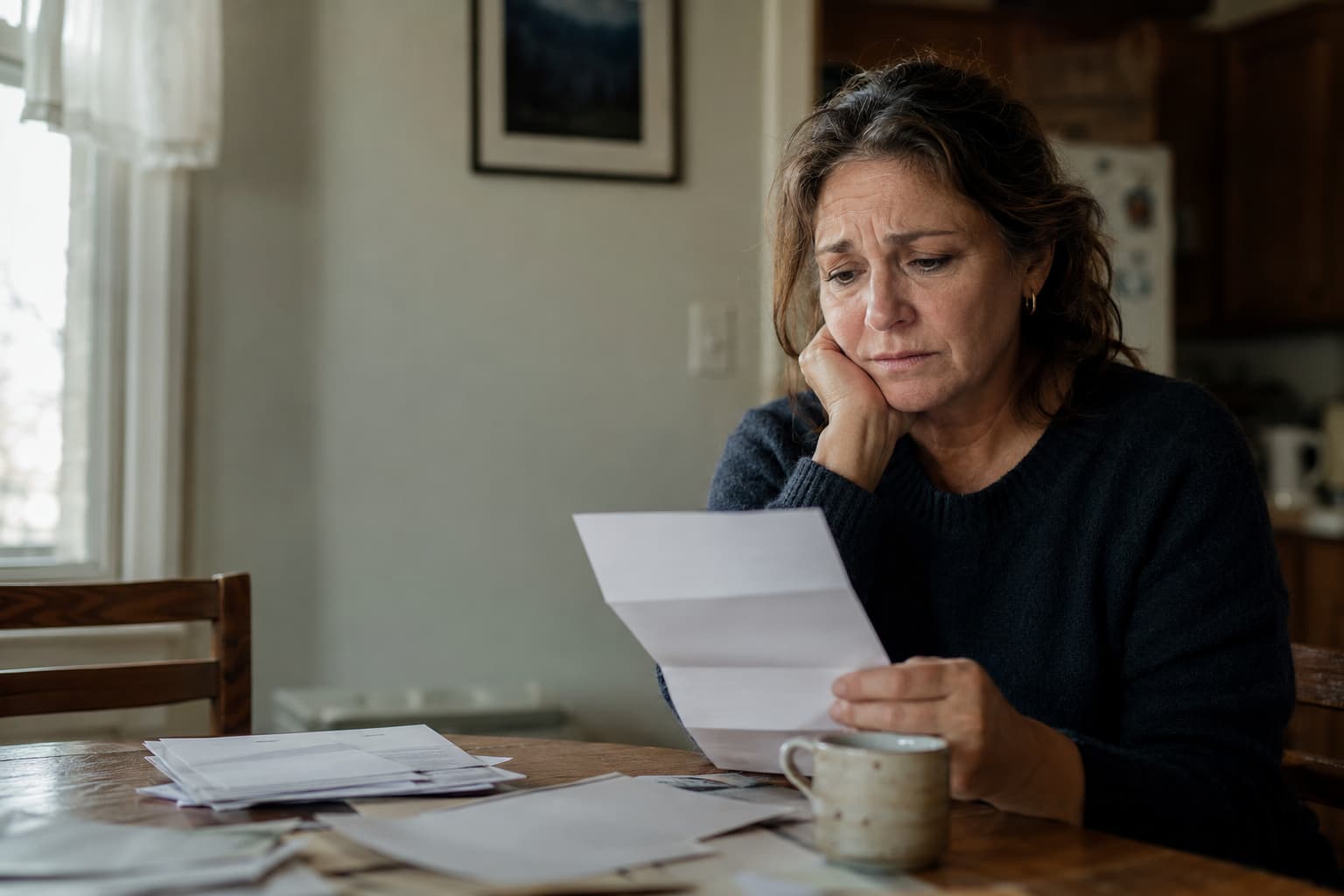

But I was lied to.

A year after my dad died, I got a bill from the state for $177,000 for his Medicaid expenses. And if that wasn't bad enough, they threatened to sue for the house if I didn't pay — the same home my dad spent his entire life working for. The same home he raised me in.

That's when I learned something nobody tells you until it's too late: if you don't do everything in your power to protect your assets, the government will do everything and anything to take them away and bankrupt you. Plain and simple.